E-commerce subscriptions are doubling every year, with Gen Z driving its snowballing popularity. Where there’s demand for subscriptions, there’s also a need for efficiency in recurring payments. CVRPs are getting significant interest share from merchants and payment service providers, making them a potential new stage in open banking progress.

Types of Recurring Payments

An average bank customer is forgetful. If they have to keep all their scheduled payments in mind, that would be a disaster. Mortgage, rent, utility bills, Netflix subscriptions, school fees, loan interest, gym membership, savings deposit, and many more transactions happen on a regular basis. Thankfully, modern technology allows people not to memorise all that. It offers automation instead. Once set, your recurring payments happen right on a schedule without much intervention. How is it technically possible? There are a few distinct payment mechanisms behind automated regular payments.

Direct Debit

Direct Debit is an automated payment method that allows a business or service provider to withdraw a set amount of funds directly from your bank account on agreed dates. Users give permission (mandate) to the company to collect payments. The payee initiates the transaction, which should be pre-authorised by the payer. If the amount changes (e.g. your utility bill increases), users are notified a few days prior to the fund withdrawal.

Standing Order

Standing orders are fully controlled and initiated by payers. They give an instruction to the bank or similar financial institution to automatically transfer a fixed amount of money from their account to another account on a regular schedule. This type of payment may occur between the same user’s accounts (regular money transfer to a savings account, round-up feature, etc.), or go from one bank user to another (paying rent, supporting charity, and so on). The amount transferred remains the same unless the user manually changes it.

Card on File

The payment method can be used for both recurring and one-time payments. The user registers with a merchant or service provider and stores the card details in-app or via the web portal for future use. The data storage requires user consent. The following purchases are made through simplified authorisation, enabling services like one-click checkout.

Credit/Debit Card Recurring Charges

A bank card is stored while subscribing to a streaming service, gym membership, or insurance policy. This payment can be of a fixed or variable amount. For instance, a streaming service may charge a set amount per month plus additional sums for exclusive extra content. The payments are automatically charged to a stored card at regular intervals.

Installments and BNPL

A bank or a fintech company breaks down a purchase sum into smaller amounts to boost its affordability for the customer. A financial institution sets a repayment plan for this type of short-time loan. Installment payments and Buy Now, Pay Later (BNPL) plans can be applied to both credit/debit cards and bank accounts, depending on the provider and offering. When using a credit card, the total amount is charged upfront, and the borrower pays it back in fixed installments, often with added interest. If linked to a bank account, the amount is automatically charged based on the agreed schedule via Direct Debit.

What Is Commercial Variable Recurring Payment (CVRP)?

Commercial Variable Recurring Payments are a subtype of variable recurring payments – regular money transfers of variable amounts. Unlike ordinary VRPs, they are not sweeping (me-to-me) transactions that are frequently used for savings or automated budgeting purposes. Instead, they take place between accounts of different users, developed specifically for enterprises that can receive flexible payments from their customers or business partners and leverage automatic recurring billing systems.

CVRPs are technically possible due to the development of open banking technology. This secure infrastructure allows third-party providers to access bank customers’ data through Application Programming Interfaces (APIs). In this scenario, a licensed third-party provider can initiate payments on behalf of the customer upon their consent. Some APIs enable bridging traditional payment rails with blockchain infrastructure, leveraging smart contracts to create programmable conditions for recurring payments from customers’ crypto wallets.

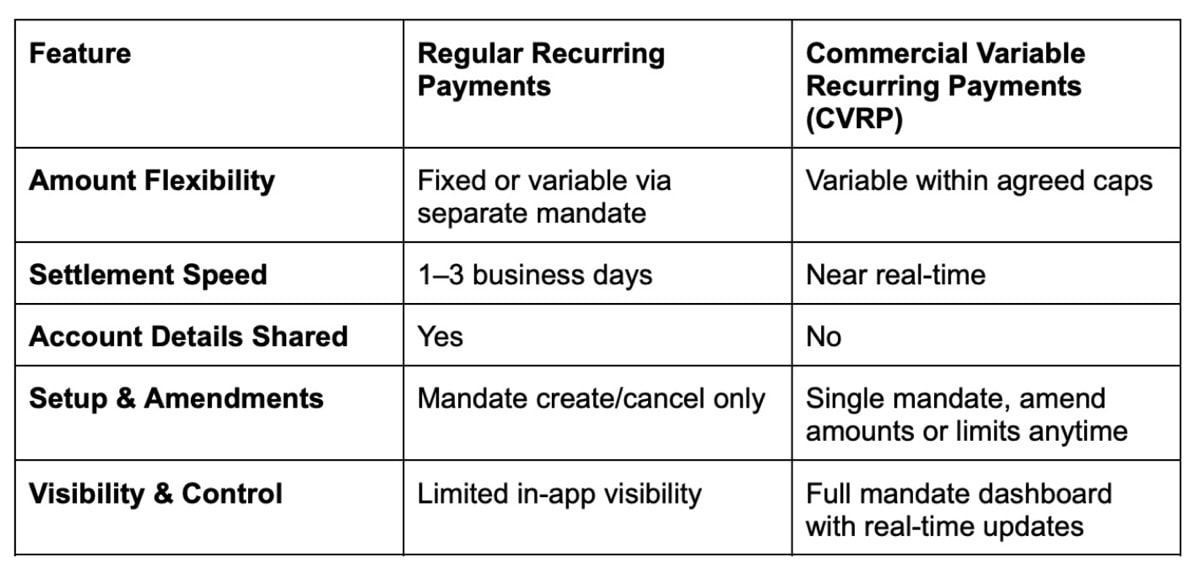

Standard Recurring Payments vs CVRPs

Unlike traditional methods used for recurring payments, CVRPs provide much greater flexibility, convenience and control to both service users and providers. Under a single authorisation, payees can collect different amounts each cycle (e.g. a utility bill that varies by consumption) up to agreed caps. Customers don’t need to re-consent each time for minor fluctuations.

Moreover, users may set both per-transaction and aggregate payment limits per period to make sure there are no overcharges. They can view, modify, or revoke CVRP mandates instantly through online or mobile banking service. Every future payment and cap is visible and transparent.

In addition, CVRPs offer more security, since businesses can pull payments directly from customer accounts without needing card-on-file systems. The less sensitive data is stored with multiple parties, the better for its safety. Such payments are authorised via secure API credentials (OAuth) so that third-party uses access tokens instead of actual customer passwords.

How CVRPs Revolutionise Open Banking

Open banking has enormously transformed the financial services industry as we know it. And yet, most countries still haven’t embraced the CVRP functionality for payments within regulated industries. When they do, they might benefit greatly.

CVRPs Enable Greater Cost-Efficiency for Businesses

One example is the UK, where banks are still not universally mandated to support premium API-based Commercial Variable Recurring Payments, but there’s already an active development of legal and commercial framework for such payments to function. Until legal obligations and unified rulebooks are in place, only 32% of local banks plan to support CVRPs for low-risk use cases in 2025.

Meanwhile, Plaid estimates that expanding the use of Variable Recurring Payments (VRPs) to commercial applications beyond sweeping could enable businesses to save more than £1.5 billion each year in payment processing costs.

To be more precise, UK businesses pay roughly £2.2 billion per year in issuer fees for card-on-file, direct debit, and recurring card payments. If VRPs in general (including commercial VRPs) were capped at 0.10% per transaction, the total annual fees across the same payment volume would drop to about £700 million.

At the same time, the report cautions regulators to introduce a cap on CVRP issuer fees to prevent banks from charging unsustainable fees that would discourage both businesses and consumers from adopting this payment method.

Reduced Failures, Chargeback and Remediation Costs

It is estimated that Direct Debits in the UK fail about 8% of the time, triggering manual retries, customer service interventions, and sometimes penalty fees. The failure reasons range from wrong sort-code or account-number details to the payer changing banks or account numbers without updating their mandate. Direct debits also sometimes miss their submission windows or are disputed by customers.

Recurring card payments and card-on-file transactions face significantly higher failure rates (between 15%-30%), as cards often expire and recurring payment instructions need manual changes.

Overall, recurring payment failures are a top concern for 41% of subscription businesses. Their employees spend about five hours each week just trying to figure out the reasons for failed payments and ways to sort that out. More than half of business owners (56%) find payment failures expensive to track and resolve.

Meanwhile, CVRPs employ real-time confirmation of account status and available balance. That translates to fewer failed payments and less staff time spent chasing the elusive failure reasons or re-billing. Moreover, every 1% reduction in failure rates could save millions in remediation costs.

Finally, CVRPs operate “account-to-account” (A2A) via Open Banking APIs. That mode of transacting eliminates not only interchange fees charged by card networks but also additional fixed/penalty fees associated with chargebacks. Every VRP transaction requires the customer to re-authenticate (e.g. via fingerprint, face ID, or banking PIN) whenever a mandate is set or modified. It virtually eliminates unauthorised or fraudulent transactions, removing the root cause of most disputes.

Customers Get Faster Frictionless Payments With Greater Visibility

Of course, merchants and payment providers are not the only ones to benefit from API-based Commercial Variable Recurring Payments. Customers enjoy the ease and speed of such transactions on the background of their slower and more cumbersome legacy counterparts.

Users can see the upcoming payments, payment limits, frequency, and the expiry date of their consent for recurring transactions. They may pause, amend, or cancel any mandate instantly in their bank’s dashboard. They do not face opaque “card-on-file” agreements where customers only spot charges after the funds are withdrawn.

CVRPs also settle immediately, with both parties of the transaction notified right away. As a result, you get a more user-centric payment experience where merchants pull exactly what’s owed, up to the agreed cap, without asking clients to re-sign every month, and get faster access to transferred funds.

Bottom Line

Commercial Variable Recurring Payments (CVRPs) are starting to gain traction in industry discussions and among local regulators. Merchants who will benefit the most from the full deployment of CVRP frameworks on national levels are most interested. It is no wonder since they’re going to see tangible financial benefits from this introduction. Meanwhile, many customers, who will surely enjoy the transparency and flexibility of CVRPs as well, still have little understanding of the next transformation in open banking they’re going to soon witness.

CVRPs promise to become a game-changer for e-commerce subscriptions, which are booming thanks to Gen Z’s influence. Unlike standard recurring payments, CVRPs allow businesses to automatically collect variable amounts directly from customer bank accounts through secure APIs, without the need for card details or constant re-authorisation. This means faster settlements, lower processing fees, and real-time visibility for both parties. Besides, compared to traditional Direct Debits and card-on-file systems, CVRPs boast fewer failed payments, no chargebacks, and better fraud protection.